The Great Simplification Meets Bold Expansion

December 2025 through February 2026 marks a turning point in ESG regulation. After years of criticism about excessive complexity and compliance costs, global regulators are pursuing a dual strategy: simplifying frameworks in established markets while expanding requirements in emerging economies. This isn't retreat, it's recalibration.

EU Omnibus: 80% Fewer Companies, Same Ambition

On December 16, 2025, the European Parliament approved the Omnibus I package, dramatically reshaping EU sustainability rules. The numbers tell the story:

CSRD Impact: From 50,000+ companies to roughly 10,000. New thresholds require 1,000+ employees and €450 million turnover, up from the original 250 employees. Data points slashed from 1,073 to 320 (70% reduction).

CSDDD Impact: Scope narrowed to 5,000+ employees and €1.5 billion turnover. Implementation pushed to July 2029. Climate transition plan requirement removed, though disclosure still required under CSRD.

Real Impact: Wave 1 companies: those required to report for 2024 faced an unexpected twist. Many started sustainability reporting only to discover they'd fall outside the new thresholds. Member States can now grant exemptions for 2025-2026, providing transition relief. Financial holding companies (like private equity firms) are completely exempted if they don't manage day-to-day operations of portfolio companies.

The Anti-Trickle-Down Protection: Companies with fewer than 1,000 employees can now legally decline information requests from larger companies in their supply chain unless they're voluntary SME standard disclosures. This protects smaller businesses from becoming unpaid ESG data providers.

Brazil's Bold Experiment: Social Justice Meets Green Finance

While Europe simplifies, Brazil is innovating. Approved in August 2025 and published via Presidential Decree No. 12,705/2025 on October 31, Brazil's Sustainable Taxonomy (TSB) is the world's first to explicitly integrate racial and gender equity alongside environmental criteria.

Coverage: Eight sectors including agriculture (which the EU Taxonomy excludes). Covers cattle, soy, corn - responsible for Brazil's largest environmental impacts. Initially covers 9 key commodities: soy, corn, cattle, coffee, cocoa, eucalyptus, pirarucu, tilapia, and tambaqui.

Deforestation Red Line: From 2030, only properties with zero deforestation in the previous 5 years qualify for green financing. This directly impacts Brazilian agribusiness, which accounts for 29% of GDP and employs 28 million people.

Social Equity First: Requirements to demonstrate contributions to racial and gender equity throughout production chains and workforce going beyond environmental metrics.

Timeline: Voluntary initially, shifting to mandatory by January 2026 for capital markets and financial institutions. Will inform credit lines, tax incentives, and public procurement decisions.

Controversy: Critics argue the focus on practices rather than measurable impacts creates greenwashing risks. The methodology's complexity and sector-specific approach (rather than cross-commodity criteria) may limit effectiveness. Yet it represents the first serious attempt to link sustainable finance with social justice outcomes.

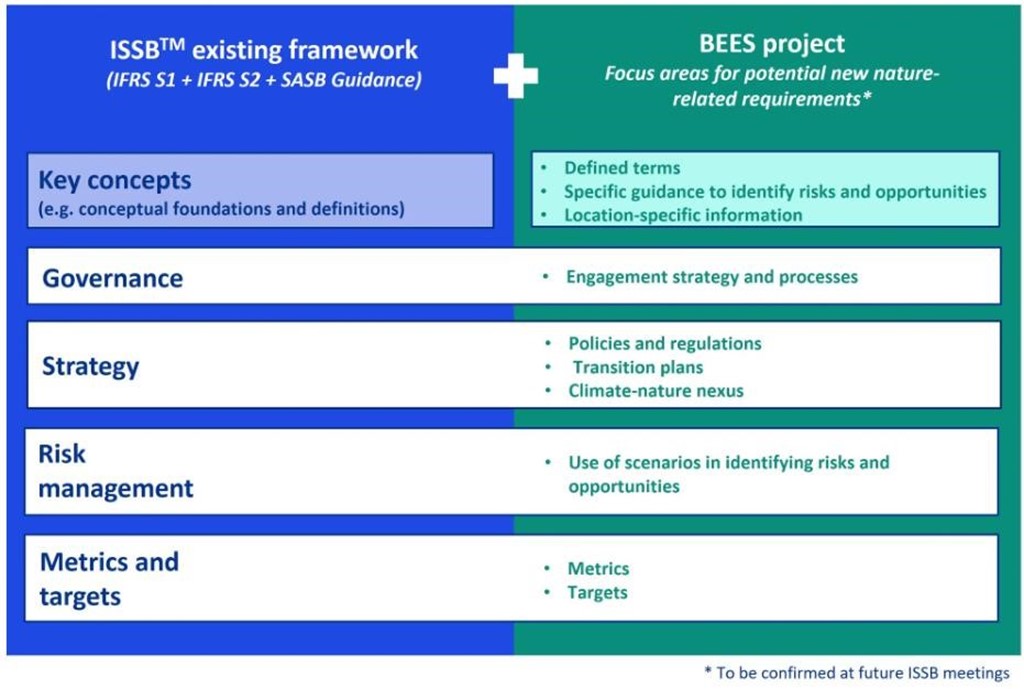

ISSB Pivots to Nature: Climate-First Era Ends

In November 2025, the International Sustainability Standards Board (ISSB) announced it will develop nature-related disclosure requirements, targeting an exposure draft by October 2026 for the Convention on Biological Diversity COP17 in Armenia.

The Foundation: Over 730 organizations representing $9 trillion in market cap and $22 trillion in AUM have committed to the Taskforce on Nature-related Financial Disclosures (TNFD) framework. TNFD will complete current work by Q3 2026, then pause to support ISSB's standardization.

What's Different from ESRS: The ISSB will integrate nature topics (land use, pollution, water, biodiversity) into existing IFRS S1 and S2 standards rather than creating separate standards.

Source: KPMG

Materiality remains financial; companies report only what affects their financial prospects, avoiding exhaustive checklists.

Preparedness Gap: Australian research in late 2025 found two-thirds of companies surveyed weren't prepared for TNFD requirements, citing limited internal awareness. Organizations should start baseline biodiversity assessments now rather than waiting for 2027 finalization.

What This Means for Your Organization

If You're in Europe: Don't assume you're exempt. Review both thresholds (employees and turnover). Companies falling outside scope face strategic choices: maintain voluntary reporting for investor confidence or scale back.

Note: review clauses mean scope could tighten again post-2029.

If You're in Latin America: Brazil's integrated environmental-social approach may influence regional frameworks. Companies in agriculture, mining, and energy sectors should assess alignment with TSB criteria now. Access to green financing and tax incentives will increasingly depend on it.

If You're Anywhere: Start nature-related risk assessments immediately. Use TNFD's LEAP approach (Locate, Evaluate, Assess, Prepare). Investor expectations are already shifting. Norges Bank Investment Management ($1.7 trillion AUM) expects companies to integrate biodiversity into strategy and risk management regardless of mandatory timelines.

The Bottom Line

ESG regulation in 2026 is consolidating and diversifying simultaneously. Europe is responding to cost concerns with higher thresholds and fewer data points. Brazil is pioneering integrated environmental-social frameworks. Global standard-setters are expanding from climate to nature.

The common thread: moving from adolescence to maturity and balancing ambition with practicality.

Organizations that view this as purely compliance risk missing the point. These changes create strategic opportunities to strengthen stakeholder relationships, access capital more efficiently, and position for the low-carbon, nature-positive economy. The question isn't whether to engage. It's how to lead.