How the IPBES Business & Biodiversity Report and TNFD Are Reshaping Corporate Accountability in 2026

The Biodiversity Wake-Up Call

For years, biodiversity was the sustainability issue that

finance and compliance teams quietly deferred to another department. Not

anymore.

In February 2026, the Intergovernmental Science-Policy

Platform on Biodiversity and Ecosystem Services (IPBES) released its landmark Business

& Biodiversity Assessment and it rewrote the terms

of the conversation. Biodiversity loss is no longer framed as an environmental

concern. It is now officially classified as a systemic risk to the global

economy.

That language matters. “Systemic risk” is the vocabulary of

central banks and financial regulators. It is the vocabulary of boards, not

just CSR reports. And it is the vocabulary that, historically, precedes

mandatory action.

|

|

|

“Nature loss is not an environmental footnote — it is a

financial stability issue.” |

|

|

The Scale of Exposure

Before diving into frameworks and timelines, it helps to

understand why the urgency is real and why regulators are paying attention.

|

|

|

|

|

$58T |

73% |

733+ organizations

across 56 countries committed to TNFD

disclosures |

Sources:

$58T — PwC Nature Risk Report (2023) / WEF New Nature Economy Report (2020),

updated figure widely cited by WWF & IPBES; 73% — WWF Living Planet Report

2024 (ZSL Living Planet Index, tracking 34,836 populations of 5,495 species,

1970– 2020); 733+ — TNFD Adopters Registry (tnfd.global)

Put

simply: if your business depends on

stable supply chains, water, agriculture, fisheries, or raw materials, it

depends on nature.

From Voluntary to Mandatory: The Regulatory Arc

The progression here follows a familiar pattern in

sustainability regulation. First come voluntary frameworks. Then reporting

expectations harden. Then disclosure becomes mandatory. We have seen it with

climate. Nature is following the same arc, only faster.

The Kunming-Montreal Global Biodiversity Framework,

adopted in 2022, set the trajectory. Target 15 specifically calls on large

companies to assess, disclose, and reduce their biodiversity impacts. The

European Union is already embedding this into domestic regulation, with

implications for any company operating in or exporting to the EU.

Meanwhile, 2026 is shaping up to be a critical platform

year for the Science Based Targets Network (SBTN), which

validated its first corporate nature targets in early 2025. The significance:

for the first time, companies have a science-grounded methodology to set

meaningful, measurable nature commitments and not just intentions.

The Taskforce on Nature-related Financial Disclosures (TNFD) provides the reporting

architecture. With over 733 organizations already signed on across 56

countries, TNFD adoption is moving rapidly from early-adopter territory into

mainstream expectation.

|

📂 Case Study:

Kering (Luxury & Fashion) Industry:

Luxury goods / fashion What they

did: Kering has been piloting biodiversity integration into its

sourcing strategy, including ecosystem impact assessments across its leather

and cotton supply chains. The company is among the early corporate adopters

testing TNFD-aligned reporting. Outcome: Kering’s

Environmental Profit & Loss (EP&L) model now captures nature-related

costs, giving the company a financial lens on biodiversity risk that goes

beyond compliance influencing sourcing decisions and supplier engagement.

|

|

|

|

📂 Case Study:

Carrefour (Retail & FMCG) Industry:

Retail / FMCG What they

did: Carrefour has been working to integrate biodiversity

metrics into its supplier assessment frameworks, particularly for high-risk

commodities like soy and palm oil. |

|

|

|

Outcome: By

mapping which product categories carry the highest nature-related risk

upstream, Carrefour has been able to prioritise supplier engagement

and set more credible deforestation-free commitments. |

|

|

ASEAN: Caught Between Hotspot and Hub

The ASEAN region faces a particular tension in this moment.

It is home to extraordinary biodiversity: the forests of Borneo, the marine

ecosystems of the Coral Triangle, the agricultural landscapes of the Mekong

Delta while also serving as one of the world’s most critical manufacturing and

supply chain hubs.

That dual role creates both exposure and opportunity. On

one hand, ASEAN-based companies supplying to European markets are increasingly

subject to the EU’s emerging nature-related disclosure requirements. On the

other, the transition to a nature-positive economy is projected to unlock

significant new value across the region in sustainable agriculture, ecosystem

services, and green finance.

Investor pressure is also intensifying. Institutional

investors are increasingly seeking integrated climate-and-biodiversity

reporting, treating nature-related risk as material to capital allocation

decisions. For ASEAN companies seeking international capital, aligning with

TNFD is rapidly becoming a market access question, not just a values question.

|

|

|

For ASEAN companies supplying to EU

markets, TNFD alignment is becoming a market access question, not just a

values question. |

|

|

The Honest Reality: Implementation Is Hard

The frameworks are multiplying. The expectations are

rising. The hard part? Making it operational.

The Nature Positive Initiative has identified over 600

different environmental metrics currently in use across

corporate reporting. That fragmentation creates genuine confusion especially

for sustainability teams trying to figure out where to start, what to measure,

and how to ensure comparability.

A major consultation on metric harmonisation ran in early

2026, with the goal of building a more consistent, credible measurement

framework. But in the interim, companies face a real risk of disclosure

fatigue: producing reports that satisfy checklists without driving real change.

The more fundamental challenge is cultural. Biodiversity

risk needs to move from sustainability departments into procurement, finance,

and boardrooms. The gap between awareness and operational decision-making

remains wide and closing it requires more than good intentions.

What Companies Should Do Now

The compliance clock is ticking but this is also an

opportunity to get ahead of the curve. Here is a practical starting framework:

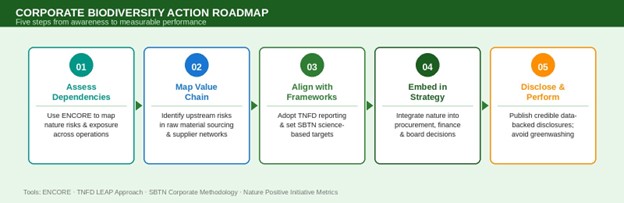

• Start with a dependency audit. Assess

your nature-related risks and dependencies using tools like ENCORE (Exploring

Natural Capital Opportunities, Risks and Exposure), which maps how business

sectors depend on and impact ecosystem services.

• Map your value chain. Identify which

parts of your value chain carry the highest biodiversity risk typically

upstream in raw material sourcing. High-risk commodities include soy, palm oil,

beef, timber, and certain minerals.

• Align with emerging frameworks. Begin

engaging with TNFD’s disclosure recommendations and explore SBTN’s corporate

nature target methodology. Even voluntary adoption now builds credibility and

prepares you for mandatory regimes ahead.

• Bring nature into the boardroom. Biodiversity

risk assessments need to inform procurement, investment, and strategic

decisions not just sustainability reports.

• Be transparent, not just optimistic. Disclose what you know and what you are working on but ensure it is backed by real data and measurable commitments. The era of narrativeonly sustainability reporting is ending.

Figure

2: Corporate biodiversity action roadmap — from initial assessment to credible

performance reporting.

A Defining Moment — If Companies Act Like It

Every major regulatory shift in sustainability has had a

defining year, a moment when the direction became undeniable and the laggards

became visible. For climate, it was the years following the Paris Agreement.

For human rights due diligence, it was the wave of national legislation through

2021-2023.

2026 may be that year for nature.

The IPBES report has given policymakers and investors the

scientific mandate. TNFD and SBTN have given companies the tools. The

Kunming-Montreal Framework has given governments the political commitment. What

remains is execution.

Nature is no longer a background condition

for business. It is becoming a foreground compliance requirement.

The companies that move now building measurement

capability, integrating nature into strategy, and reporting with credibility

will be far better positioned than those waiting for mandatory deadlines to

force their hand.

Key

References & Further Reading

IPBES

Business & Biodiversity Assessment media release:

https://www.ipbes.net/bba-report/media-release

IUCN

response to IPBES report:

https://iucn.org/news/202602/ipbes-business-and-biodiversity-report-highlightscollaboration-needed

CouncilFire

— Nature-positive corporate strategy:

https://www.councilfire.org/blog/nature-positive-businessbiodiversity-integrating-nature-into-corp…

Dunya

Analytics — Why 2026 is nature’s breakthrough year: https://www.dunya-analytics.com/insights/why-2026could-be-natures-breakthrough-year-for-business

Nature

Positive Initiative — Metrics: https://www.naturepositive.org/metrics/

TNFD

Adopters Registry: https://tnfd.global/engage/tnfd-adopters/