EXECUTIVE SUMMARY

• EV Market 2025: BYD overtakes Tesla (2.26M

vs 1.64M Battery Electric Vehicle (BEVs)) | 30M+ global EV sales | China 60%

market share

• Battery Supply: $15.8B raw materials spend

| Lithium-nickel-cobalt demand surging | China 90%+ processing dominance

• Renewable Energy: 4,600 GW capacity

additions by 2030 | Solar 80% of growth | Renewables to overtake coal in

2025-2026

• Nuclear Renaissance: SMRs emerging | 312.5 MW→912.5 MW by 2030 | First commercial deployments starting

Part 1: Electric Vehicles – The Reality Check

Market Shake-Up: China's BYD Dethrones Tesla

In 2025, the global EV market witnessed a

historic power shift: BYD sold 2.26 million battery electric vehicles, crushing Tesla's 1.64 million

deliveries and claiming the crown as the world's largest EV manufacturer. This

marks Tesla's first annual sales decline (down 9%) and ends its multiyear

dominance. BYD's victory wasn't

just about volume, it reflects a strategic master class in affordability,

diversification, and global expansion.

The table below captures the top four

global electric vehicle manufacturers by sales volume in 2025, highlighting a

historic shift in market leadership. The data shows each manufacturer's market

share, year-over-year growth trajectory, and their relative positioning in a

rapidly expanding global EV market that surpassed 30 million total units in

2025.

|

Manufacturer |

Market Share |

YoY Growth |

|

|

BYD

(China) |

2.26M BEVs |

19.9% |

+28% |

|

Tesla

(USA) |

1.64M BEVs |

7.7% |

-9% |

|

Geely

(China) |

845K |

5.6% |

+238% |

|

VW Group |

420K |

2.8% |

+32% |

Total Global EVs (including PHEVs): 30+ million units sold in 2025 (+20% YoY)

Inside an EV: Critical Battery Components

EV batteries are technological marvels and

supply chain nightmares. A typical lithium-ion battery pack contains:

|

Component |

Function |

Supply Concern |

|

Lithium |

Powers energy storage in the cathode, with most global

demand now driven by batteries |

China dominates refining and processing |

|

Nickel |

Increases energy density, enabling longer driving ranges |

Indonesia's export policies and tight supply create price

volatility |

|

Cobalt |

Ensures battery stability and longevity |

The majority comes from the Democratic Republic of Congo,

raising persistent ethical concerns about mining practices |

|

Graphite |

Serves as the anode material |

China controls nearly all processing capacity, creating

strategic supply risks |

|

Manganese |

Provides structural integrity and power output |

Global supplies remain constrained |

EV Costs: The Path to Price Parity

Battery pack prices have dropped

dramatically over the past decade, approaching the critical threshold where EVs

can compete with gasoline vehicles on price alone without subsidies. In China,

entry-level electric models already cost less than comparable gas cars, proving

that scale manufacturing can deliver affordable EVs.

Western markets tell a different story.

The expiration of federal tax credits and high tariffs on Chinese imports

protect domestic manufacturers but keep consumer prices elevated. The result:

EVs remain premium purchases in the US and Europe, while China has achieved

genuine mass-market adoption. The path to affordable EVs exists but policy and

trade barriers determine who gets to drive it.

Part 2: Renewable Energy – The Future is Solar (and Wind, and Nuclear)

The Solar Surge: 4,600 GW by 2030

Global renewable power capacity is set to

double by 2030, adding 4,600 GW equivalent to combining China, the EU, and

Japan's entire power generation capacity. Solar photovoltaic accounts for 80%

of this growth, driven by plummeting costs (now the cheapest new generation in

most countries), faster permitting, and broad social acceptance.

|

Renewable Milestone |

Status / Projection |

|

Renewables overtake coal as largest electricity source |

End of 2025 / Mid-2026 |

|

Renewable share of global electricity generation |

32% (2024) → 43% (2030) |

|

Solar PV capacity growth 2025-2030 |

More than

doubles |

|

732 GW (+45% vs 2019-2024) |

|

|

140 GW (2025-2030) |

|

|

China's share of global renewable additions |

60% |

Source: IEA Renewables 2025 Report

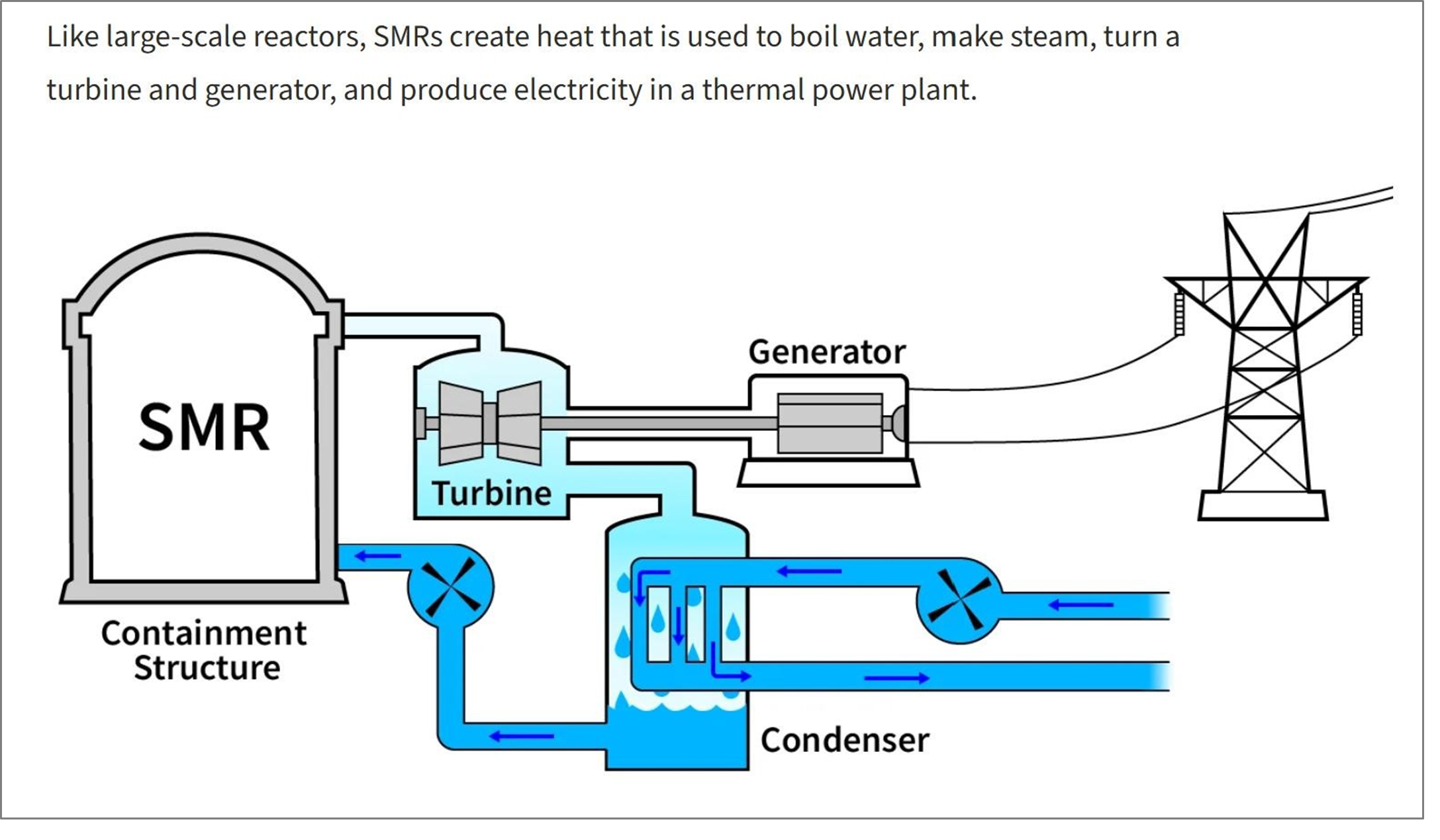

Nuclear Renaissance: Small Modular Reactors (SMRs)

While renewables dominate headlines,

nuclear energy is experiencing a quiet renaissance. Over 40 countries now

support nuclear expansion, driven by energy security concerns and 24/7 baseload

needs that intermittent renewables can't meet alone. The gamechanger: Small

Modular Reactors.

What are SMRs?

Factory-built reactors (50-350 MW

capacity) that are smaller, simpler, and faster to deploy than conventional

nuclear plants.

Key advantages: 60% lower capital costs, 24–36-month construction timelines, passive safety systems, and suitability for remote locations or industrial facilities.

Source: https://understand-energy.stanford.edu/news/understand-small-modular-reactors

Source: https://understand-energy.stanford.edu/news/understand-small-modular-reactors

Market Trajectory: SMR installed capacity: 312.5 MW (2025) → 912.5 MW (2030)

at 23.9% Compound Annual Growth Rate (CAGR). First

commercial projects coming online 2030 (TerraPower Natrium in Wyoming, X-energy

Xe-100 at Dow Seadrift). Tech giants are major customers: Google signed 500 MW

with Kairos Power; Amazon investing in Xenergy and Energy Northwest projects

totalling 5 GW.

The Nuclear-Renewable Synergy: Nuclear provides baseload stability; renewables provide variable capacity. Together, they enable deep decarbonization. IEA projects nuclear capacity must reach 1,160 GW by 2050 (from 394 GW in 2020) to meet 1.5°C climate targets. SMRs bridge the gap where large reactors face public opposition or insufficient grid capacity.

The Integration Challenge: EVs, Grids, and Renewables

Here's the trillion-dollar

question: How do we power 30 million+ EVs with clean electricity when solar/wind are intermittent and grids are

constrained? The

answer involves three simultaneous transformations:

1. Grid Expansion

UK example: Scotland generates most wind

power; demand is in the south.

Result: £1.4B paid to wind farms in 2023

to NOT produce electricity due to transmission constraints. UK grid operator

estimates £40B/year investment needed through 2030. US, EU face similar

bottlenecks.

2. Energy Storage

Battery storage deployment hit 1 TWh

capacity in 2025. Pumped hydro (using excess renewable power to pump water

uphill, then generating electricity on demand) growing 80% faster 2025-2030 vs

previous period. Vehicle-to-grid (V2G) technology turns EV batteries into

distributed storage but requires bidirectional charging infrastructure rollout.

3. Flexible Baseload

Natural gas provides dispatchable power but emits CO2. Nuclear (including SMRs) provides carbon-free baseload. Hydrogen electrolyzers can absorb excess renewable generation, producing green hydrogen for industry/transport. Geothermal (projected to triple by 2030) offers 24/7 renewables.

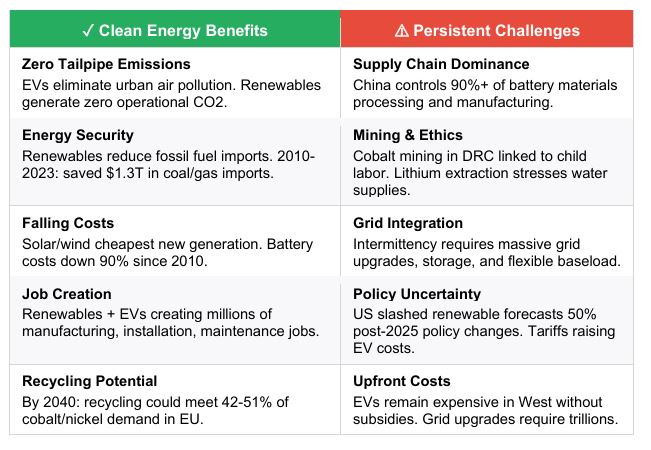

Benefits vs. Challenges: The ESG Scorecard

The Bottom Line: Transformation Underway, But Not Without Friction

The clean energy transition is no longer

theoretical, it's happening at scale. BYD manufactures 2.26 million EVs

annually. Solar PV capacity is doubling by 2030. Renewables are overtaking coal

as the world's largest electricity source. Battery costs have dropped 90% in a

decade. Nuclear is staging a comeback via SMRs.

But success isn't guaranteed. Supply

chains remain concentrated in China. Mining ethics are unresolved. Grids need

trillions in upgrades. Policy whiplash threatens momentum. And the transition

timeline reaching net-zero by 2050 requires doubling current deployment rates.

For ESG investors and corporate

strategists, the message is clear: The energy transition is the largest

infrastructure buildout in human history. Winners will be companies that solve

supply chain bottlenecks, scale manufacturing, and navigate policy volatility.

Losers will be those who treat sustainability as compliance theatre rather than

competitive strategy.

“The future is

electric. The future is renewable. The question isn't if, but how fast and who

captures the value along the way.”