In a world increasingly shaped by climate imperatives, stakeholder scrutiny, and regulatory momentum, the International Standard on Sustainability Assurance 5000 (ISSA 5000) emerges as a game-changer. Developed by the International Auditing and Assurance Standards Board (IAASB), ISSA 5000 sets a global baseline for credible, consistent, and comparable assurance of sustainability disclosures—across frameworks, industries, and jurisdictions.

🔍 What Is ISSA 5000?

ISSA 5000 is the first comprehensive international standard dedicated solely to sustainability assurance. Unlike its predecessor ISAE 3000, which was broader and less tailored, ISSA 5000 zeroes in on the unique challenges of ESG reporting, including:

- Double materiality (financial and impact)

- Forward-looking disclosures

- Value chain data

- Limited and reasonable assurance levels

It is framework-neutral, meaning it can be applied to disclosures prepared under GRI, IFRS S1/S2, CSRD/ESRS, SEC climate rules, or even entity-developed criteria. It’s also profession-agnostic, allowing both accountants and non-accountant assurance providers to use it—provided they meet ethical and quality management standards.

📘 “ISSA 5000 is designed to work in every jurisdiction, for a wide range of engagements, by a diversity of practitioners.”

— Tom Seidenstein, IAASB Chair

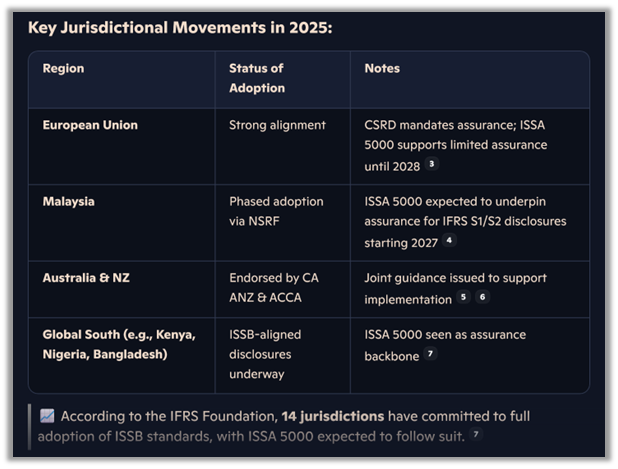

🌐 Jurisdictions Affected by Mandatory Adoption and Disclosure

While ISSA 5000 is not a regulation itself, it is rapidly becoming the de facto global benchmark for sustainability assurance. Several jurisdictions are aligning their national requirements with ISSA 5000, especially in response to the EU’s Corporate Sustainability Reporting Directive (CSRD) and the IFRS Sustainability Disclosure Standards.

📅 Effective Date and Key Details

ISSA 5000 is effective for assurance engagements on sustainability information reported for periods beginning on or after 15 December 2026. However, early adoption is permitted, and many organizations are already preparing for implementation in 2025.

Key Features of ISSA 5000:

- 212 requirements—more than double those in ISAE 3000

- Covers limited and reasonable assurance

- Applies to group and value chain disclosures

- Requires practitioner materiality aligned with entity’s double materiality

- Includes example assurance reports for different levels of assurance

Implementation Support

To ease adoption, IAASB and IESBA have released:

- Joint FAQs on ISSA 5000 and IESSA

- Example assurance reports

- Guidance on materiality and risk assessment

Case Study: Materiality in Practice

In July 2025, ACCA and CA ANZ published a guide titled “Demystifying Materiality in Accordance with ISSA 5000”. It walks practitioners through a fictional assurance engagement on Scope 1, 2, and 3 GHG emissions, highlighting how to apply professional judgment and document decisions.

🧠 “Materiality is no longer a buzzword—it’s the backbone of credible sustainability assurance.”

— Amir Ghandar, CA ANZ Reporting & Assurance Leader

💡 Why It Matters

With greenwashing risks, investor demands, and regulatory scrutiny on the rise, ISSA 5000 offers a trusted framework to validate sustainability claims. It’s not just about compliance—it’s about building confidence, comparability, and credibility in ESG disclosures.

Whether you're a listed company in Kuala Lumpur, a multinational in Frankfurt, or a sustainability consultant in Nairobi, ISSA 5000 is your passport to global assurance excellence.

🔗 Join the ESG Business Institute

🔗 Reference Links